- Register

- Sign In

Alberta Government Grants & Rebates

How to Use the First Home Savings Account (FHSA) to Buy Your First Home

The Ultimate Guide to Canada’s First Home Savings Account (FHSA) Start Saving for Your First Home Today with Canada’s FHSA Buying your first home is an exciting milestone, but the financial hurdles can feel overwhelming. That’s where Canada’s First Home Savings Account (FHSA) comes in—a groundbreaki

Read More

TFSA vs. FHSA: Which is Better for First-Time Homebuyers?

TFSA vs. FHSA: Which is Better for First-Time Homebuyers? When it comes to saving for your first home in Canada, two powerful tools stand out: the Tax-Free Savings Account (TFSA) and the First Home Savings Account (FHSA). Both offer significant tax benefits and can accelerate your journey to homeown

Read More

Easy Canadian Home Buyer’s Guide (Focused on Alberta & Saskatchewan) – Steps, Programs & Tips

First-Time Home Buyer’s Guide to Alberta & Saskatchewan Buying your first home is a big deal—especially in provinces like Alberta and Saskatchewan, where you’ll find a balance of affordability, government programs, and diverse housing options. Below is a step-by-step look at how the home-buying proc

Read More

Maximize Your First Home Savings: Combining FHSA, TFSA, and HBP for Homeownership in Canada

Maximize Your First Home Savings: Combining FHSA, TFSA, and HBP for Homeownership in Canada Buying your first home is a significant milestone, but saving enough for a down payment can feel overwhelming. Thankfully, Canadians have access to three powerful tools to make homeownership more accessible

Read More

The Home Buyers’ Plan Explained: A Guide for Alberta’s First-Time Homebuyers

The Home Buyers’ Plan: A Guide for Alberta’s First-Time Homebuyers Buying your first home can be a financial challenge, but the Home Buyers’ Plan (HBP) offers a smart solution for Canadians, including those in Alberta. This federal program allows you to withdraw up to $35,000 tax-free from your RR

Read More

Government Grants for First-Time Homebuyers in Alberta: Your Ultimate Guide

Comprehensive Guide to Government Grants for First-Time Homebuyers in Alberta Buying your first home can feel overwhelming, especially with rising housing costs. Alberta offers several government grants and programs that can help first-time homebuyers make homeownership more accessible. Here’s wha

Read More

MORE READING

- Things to do in Saskatoon this summer June 2025 Edition

Saskatoon in Full Swing: Your Ultimate Guide to June 2025 Events! June 2025 is bursting with energy in Saskatoon! If you're looking for exciting things to do, you've come to the right place. To help you make the most of this vibrant month, we’ve curated a guide to some of the best festivals, concert

Saskatoon in Full Swing: Your Ultimate Guide to June 2025 Events! June 2025 is bursting with energy in Saskatoon! If you're looking for exciting things to do, you've come to the right place. To help you make the most of this vibrant month, we’ve curated a guide to some of the best festivals, concert - How to Get a FREE Smart Thermostat: Your Guide to SaskPower's Energy Assistance Program

How to Get a FREE Smart Thermostat: Your Guide to SaskPower's Energy Assistance Program Are you a Saskatchewan homeowner looking to save money on your energy bills? Here's some exciting news: SaskPower's Energy Assistance Program is offering FREE smart thermostats to eligible households! As your loc

How to Get a FREE Smart Thermostat: Your Guide to SaskPower's Energy Assistance Program Are you a Saskatchewan homeowner looking to save money on your energy bills? Here's some exciting news: SaskPower's Energy Assistance Program is offering FREE smart thermostats to eligible households! As your loc - Calgary Real Estate Market Segments: What's Hot, What's Not (Jan 28, 2025)

Calgary Real Estate Market Segments: What's Hot, What's Not (Jan 28, 2025) Key Market Update Interest rate announcement tomorrow (Jan 29, 2025)! Follow @nasahctus for live segment-by-segment impact analysis. Current Segment Performance Detached Homes (Market Leader) 85% of inventory above $600,000 S

Calgary Real Estate Market Segments: What's Hot, What's Not (Jan 28, 2025) Key Market Update Interest rate announcement tomorrow (Jan 29, 2025)! Follow @nasahctus for live segment-by-segment impact analysis. Current Segment Performance Detached Homes (Market Leader) 85% of inventory above $600,000 S - Calgary Real Estate: Strategic Seller Guide (Jan 28, 2025)

Calgary Real Estate: Strategic Seller Guide (Jan 28, 2025) Breaking Market News Interest rate update coming tomorrow (Jan 29, 2025)! Follow me on Instagram @nasahctus for live updates and market impact analysis. Critical Market Stats Detached home median prices up 4.5% year-over-year 85% of detached

Calgary Real Estate: Strategic Seller Guide (Jan 28, 2025) Breaking Market News Interest rate update coming tomorrow (Jan 29, 2025)! Follow me on Instagram @nasahctus for live updates and market impact analysis. Critical Market Stats Detached home median prices up 4.5% year-over-year 85% of detached - Calgary Housing Market Update 2025 (Jan 28, 2025)

Calgary Housing Market Update 2025 (Jan 28, 2025) Breaking Market News: Interest rate update coming tomorrow (Jan 29, 2025)! Follow me on Instagram @nasahctus for live updates and market impact analysis. What You Need to Know Right Now:- This week's sales are significantly outpacing last week- Prope

Calgary Housing Market Update 2025 (Jan 28, 2025) Breaking Market News: Interest rate update coming tomorrow (Jan 29, 2025)! Follow me on Instagram @nasahctus for live updates and market impact analysis. What You Need to Know Right Now:- This week's sales are significantly outpacing last week- Prope - Understanding CMHC MLI Select Terms: DSCR, LTV, NOI, Cap Rate, and More

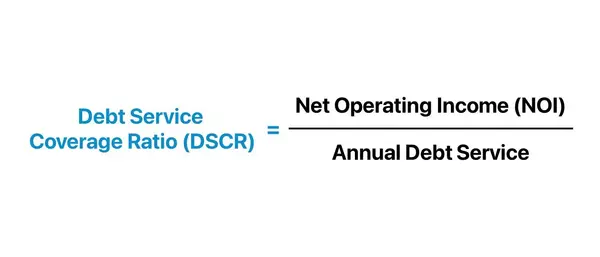

Understanding CMHC MLI Select Terms: DSCR, LTV, NOI, Cap Rate, and More Navigating the world of multi-unit residential financing can be daunting, especially when dealing with the CMHC MLI Select program. To make informed decisions and maximize your investment returns, it's crucial to understand the

Understanding CMHC MLI Select Terms: DSCR, LTV, NOI, Cap Rate, and More Navigating the world of multi-unit residential financing can be daunting, especially when dealing with the CMHC MLI Select program. To make informed decisions and maximize your investment returns, it's crucial to understand the - How to Buy Multi-Million Dollar Properties with 5% Down: The CMHC MLI Select Program (2025 Guide)

How to Buy Multi-Million Dollar Properties with 5% Down: The CMHC MLI Select Program (2025 Guide) Investing in multi-million dollar properties with just 5% down is no longer a pipe dream—thanks to Canada's CMHC MLI Select Program. Designed for investors eyeing large multi-unit residential buildings,

How to Buy Multi-Million Dollar Properties with 5% Down: The CMHC MLI Select Program (2025 Guide) Investing in multi-million dollar properties with just 5% down is no longer a pipe dream—thanks to Canada's CMHC MLI Select Program. Designed for investors eyeing large multi-unit residential buildings,